How often do you check your credit score? If you’re like me, probably only when you need to apply for a loan – which isn’t the best strategy!

After a credit discussion with a friend last week I decided to check mine.

I’ll admit, I was a bit nervous. After not checking it for so long I didn’t know what to expect.

I entered my data, loaded the page, and BOOM…

823

What?!

While I expected my score to be good, I didn’t know that it was going to be that good. I did it. I finally made it into the 800 credit score club. And here’s the thing – everything that I’ve been doing is basic. Super basic, in fact.

If you, too, want to break the 800 mark, or just improve your credit score, I’m going to tell you exactly what I’ve done so you can try it, too.

Your Credit Score – It’s More than Just a Number

Before we get down to the nitty gritty of improving your credit score, I think it’s important to cover why it matters.

Some financial gurus will argue that your credit score doesn’t matter. I think this is horrible advice and that your credit score matters very much. Here’s why:

Interest Rates – I’m sure that at some point in your life you’re going to take out a loan. The interest rate on the loan you get can make a massive difference in the amount you pay. While this is true for ALL loans it’s especially important for a mortgage.

Here’s an example:

Sally has mediocre credit. She gets a $100,000 mortgage, on a 30-year term at 7.5%. Over the life of her loan Sally pays a total of $252,000 – $152,000 of that is interest!

Sandy has great credit. She gets a $100,000 mortgage, on a 30-year term at 4%. Over the life of her loan Sandy pays a total of $194,000 – $94,000 of that is interest.

Since Sally doesn’t have the best credit, she ends up paying an extra $58,000 in interest. That’s a lot of money.

Insurance – Did you know that your credit score can play a big role in your home and auto insurance premiums? I didn’t know this until I got a job as a personal line’s insurance agent. I was SHOCKED to see just how big of an impact a credit score can have.

If you have a good driving record and claims history, but your home or auto insurance premium is still high, chances are it could be your credit score.

Rental Applications – In competitive markets your credit score can be the deciding factor in getting a rental home. After all, your credit score is often looked at as a sign of your dependability.

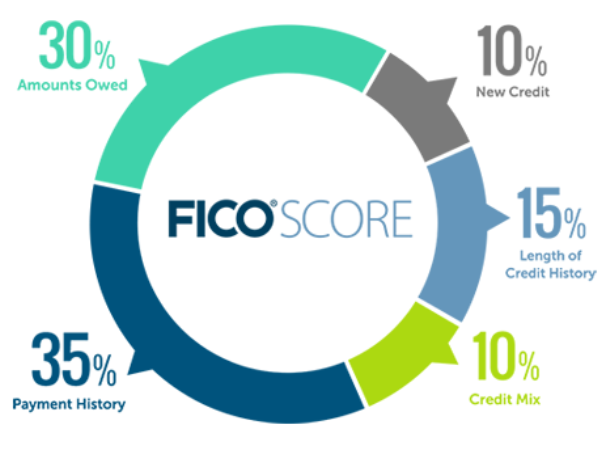

How Your Credit Score is Calculated

Before you can work on raising your credit score you need to know how it’s calculated. According to the Fair Isaac Corporation here’s how your score is calculated:

- Payment History – 35%

- Amount Owed – 30%

- Length of Credit History – 15%

- New Credit 10%

- Credit Mix 10%

So, while all five of these factors are important you can get the most bang for your buck by focusing on the first two.

Here’s what to do…

# 1 – Pay Your Bills on Time **Most Important**

Seriously, how easy could this be? This is the number one thing that is affecting your credit score.

Want to keep your credit score high? Pay your bills on time.

Have trouble paying your bills on time? Set up autopayment.

A whopping 35% of your credit score is determined by your payment history. Paying your bills on time, every month is the number one thing you can do to keep your score in good standing.

# 2 – Keep Your Credit Utilization Rate Low

The second biggest factor in determining your score is your credit utilization rate. This mainly has to do with your revolving credit (i.e. credit cards) and how much you’re charging on them verses how much credit you have available.

While there are no hard and fast rules it’s often advised to keep this ratio below 30%.

That means if you have a credit card with a $10,000 limit you don’t want to charge more than $3,000 to it.

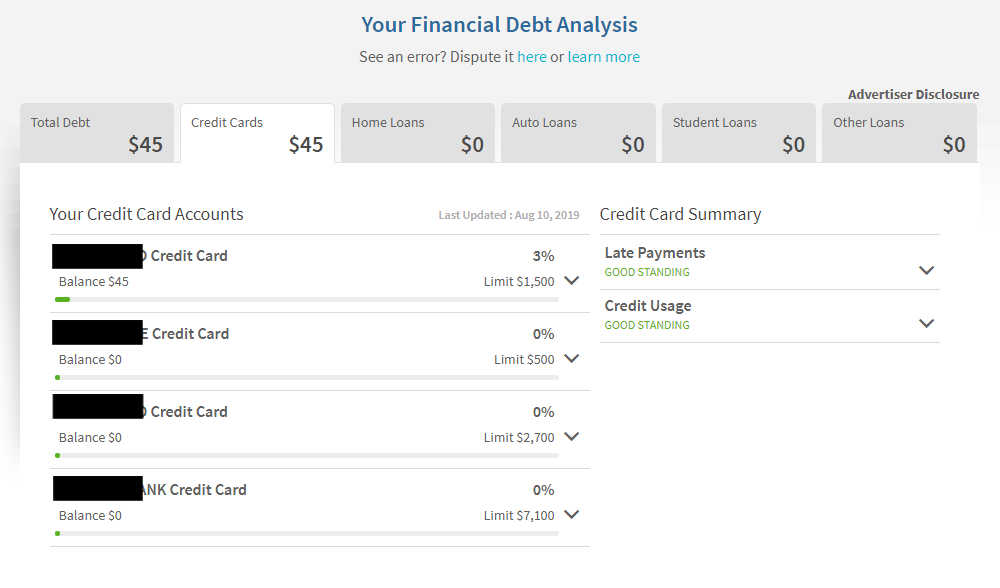

My credit utilization is much, much lower. Every month I have a $45 bill that is automatically paid via a credit card which then gets paid in full each month.

Here’s a screenshot from my Credit Sesame account:

I’m using 3% on one credit card and $0 on all the others. In other words, my credit utilization is ultra low.

If you have a Credit Sesame account you can login and click on the credit cards tab under the debt section to see your utilization percentage. (They also figure your debt to income ratio.)

If you don’t have a Credit Sesame account you can sign up for one here. They’re free. (Full disclosure: That’s my affiliate link.)

# 3 – Don’t Take Out Credit for the Sake of Taking Out Credit

Your credit mix is the combination of different types of credit you have. This could be credit cards, car loans, a mortgage, etc. And while your credit mix does count for something (10% of your credit score, to be exact) you should not take on new credit for the sake of improving your credit mix.

While I do think it’s beneficial for you to have a credit card that you charge a small amount on and payoff every month I don’t think it’s advisable to take on new credit in other forms just to improve your score. Instead, let it happen naturally. When you need a loan, take one out. But don’t do it just for the sake of raising your credit score.

# 4 – Give it Time

And lastly, you have to give it time.

Ten years ago I barely qualified for a car loan and what I did qualify for didn’t come with a very good interest rate. Now I could qualify for just about any loan I applied to with the best interest rates. And all I did was super simple stuff that really paid off over time.

Keep it Basic, Keep it Consistent

The bad news: there’s no magic button that will automatically raise your credit score for you. The good news: improving your credit score is pretty darn basic.

Sure,making it into the 800 credit score club will take time but all you need to focus on is 1) paying your bills on time and 2) keeping your balances low. Beyond that just stay consistent and only take out loans when you need them.