Figuring out what you should be saving for retirement can be confusing. Like, really confusing. Especially since there are a gazillion different methods for coming to that final number.

Figuring out what you should be saving for retirement can be confusing. Like, really confusing. Especially since there are a gazillion different methods for coming to that final number.

I prefer to keep things simple. Making retirement calculations complex is a fast way to keep people from figuring out what they need to save.

Today I present to you the easiest way to figure out what you need to save for retirement and why it works.

But first, just a little obligatory disclaimer: I’m not a financial advisor – just a personal finance nerd trying to explain this to the best of my ability. Consult a financial advisor for your investing and/or retirement needs.

The 4% Safe Withdrawal Rate

The 4% safe withdrawal rate. I’m sure you’ve heard of it, but do you understand what it means?

This rule states that you should be able to safely withdraw 4% of your portfolio for at least 30 years if 50% or more of your portfolio is invested in stocks.

To figure out what number you need to make the 4% withdrawal rule work for you, simply multiply what you want to spend in retirement on a yearly basis by 25.

Let’s say you want to spend $30,000 per year in retirement.

$30,000 x 25 = $750,000

As you can see you would need to have $750,000 for retirement in order for this to work. (This particular calculation is not taking social security or any other retirement income into consideration.)

Here’s why this works…….

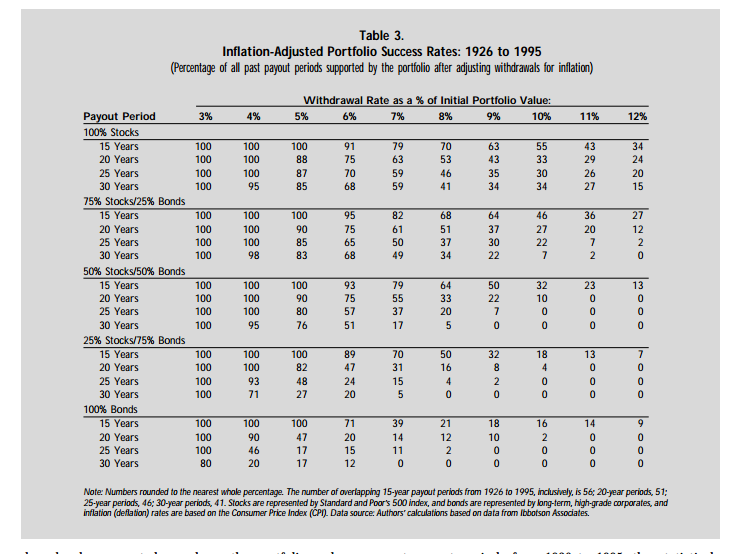

In the late 90’s three professors from the University of Trinity ran a retirement study to determine sustainable withdrawal rates for different scenarios and asset allocations. The Trinity Study found that those with a portfolio of at least 50% in stocks could withdrawal 4% per year, adjusted for inflation, with a 95% success rate of lasting at least thirty years.

The Trinity study ran thirty year periods between 1926 and 1995 to come up with this data. And remember, there were a lot of hard financial times in that range. Like the Great Depression, for instance.

(See the table above for different success rates based on different withdrawal rates.)

Income Sources That May Allow You to Save Less

If saving 25 times your annual spending sounds a little overwhelming don’t freak out yet. There are other things you may want to take into consideration.

For one, if you live in the US and have been paying into social security you’ll receive some sort of social security payment as early as age 62. (Although to get 100% of your monthly benefits you’ll have to wait until age 66 which is considered “retirement age” by the social security administration.)

The average social security benefit as of June 2015 was $1,335 per month or $16,020 per year. (Source) If you waited until age 66 to retire and received the average benefit amount it would lower your retirement income needs to an extra $13,980 per year if you were aiming for $30k per year. In this instance you’d only need to save $349,500. ($13,980 x 25 = $349,500)

Aside from social security you can also take into consideration any rental, business, or miscellaneous income you may receive in retirement.

What if You Want to Retire Early?

Want to retire early? You’re obviously not going to be getting any money from Uncle Sam until you’re at least age 62. (And by then who knows what the social security payout will actually be…)

If you want to retire early the best option is to save more money and choose a smaller withdrawal rate. If you decided you were comfortable with a 3% withdrawal rate you’d need a nest egg of 33 times your annual projected retirement spending.

Other income producing assets like rental properties or business income could also help to exponentially speed up the early retirement process.

One more important thing to note: compound interest. The sooner you get started saving the more time your money will have to compound. (This means you’re interest will start earning interest!)

Compound interest gives your money earning power which is a great help when it comes to saving those big amounts of money.

New to Saving?

If you haven’t started saving for retirement yet you’ve still got time. And if you’re confused on how to get started let me introduce you to my best friend – Betterment.

(Wait, back up a minute. If you have a 401k at work and your employer offers a match, take advantage. Start there. Sign up. Contribute what you can. If you don’t have an employer sponsored retirement plan here’s how to start a retirement account yourself…)

In my freelance career I’ve had the opportunity to test out several of the top investing services. Betterment is hands down my favorite. It has all kinds of useful tools, is super easy to use, and does the hard work for you.

If you want to start an account here’s what to do….

- Go to Betterment

(affiliate link) and sign up for an account.

- Choose between a Roth IRA or Traditional IRA (read about these choices)

- Take a short risk assessment quiz

- Based on your risk profile Betterment will select low cost ETF’s to invest in for you (you can manually adjust your risk profile if you aren’t comfortable with what they assigned you)

- Choose an initial deposit amount (there’s no minimums!!)

- Select a monthly auto-deposit amount (I suggest at least $100/month)

While you’re there you should also utilize their retirement calculator tool and play around with the numbers. There’s lots of cool stuff there to check out.

You can get your account up and running in under twenty minutes and you’ll be a touch closer to your retirement goals.

To Sum It All Up….

To figure out how much money you’ll need for a thirty year retirement simply multiply your expected retirement expenses by 25. From there you can subtract income you expect to receive from social security (if applicable) or other sources to determine what you actually need to save.

Do you know your retirement number?

So often we see articles that claim we need a million bucks per person to retire… This is mu;ch more practical. Plus, if your house was paid off, you could easily live on two thousand a month. Well, I could. ; )

~ C

Yeah I definitely could too. I don’t require much money 🙂 That’s why I my main goal is to pay off the mortgage.

I ran some numbers few days ago and we’d need about 300k Euro/each for a longer retirement. This means 600K, which is a truckload of money. On the other hand, we’re probably gonna have an active retirement, since we both work from home and it doesn’t really feel like work anyway 😀

That’s how I feel 🙂 If I was retired early I’d still be doing EXACTLY what I’m doing now so thus far early retirement just hasn’t been too big of a priority.